Time Series Forecasting Lab (Part 6) - Stacked Ensembles

B

Avec curiosité et humilité, je partage ici mes explorations en IA, data science et au-delà. Un carnet de bord pour apprendre, douter, comprendre — loin du buzz, proche du vrai.

Search for a command to run...

Hi Boris Guarisma, thank you for a great tutorial, this is the most comprehensive guide to TS forecasting in R that I've come across. Is it possible for this code to be run on a spark cluster rather than locally? Thanks again.

Hi, forecast_stacking_tbl is also missing.

It's there :-)

forecast_stacking_tbl <- bind_rows(lforecasts)

Thanks anyway !

Boris Guarisma but it is used in lapply before the bind_rows.

Simona Jokubauskaite yes, my bad, I've skipped an important part, the article has been updated. It was my last article ... I was getting tired. Thanks !

Boris Guarisma Thanks for you great work! I really appreciate it :)

Hi Boris, From where comes submodels_resamples_kfold_tbl in 'Time Series Forecasting Lab (Part 6) - Stacked Ensembles' ? I'm currently using time_series_cv(), which seems to be wrong. Could you provide the complete script in cronological order e.g. on Github? https://github.com/guzu92/courses

Hi John, thank you for your message. Indeed, I forgot to explain how the resampled predictions are obtained, I have inserted a new code snippet above, see "Generate predictons for meta-learners". Use function modeltime_fit_resamples() which uses the k-fold resamples from vfold_cv().

Boris Guarisma Hello, this is different from Matt's documentation pages. I never attended his labs and have to compare/test your code against my self-thought construction. Till now, I get different .resample_results objects per model and therefor not all predictions for the metalearner. Thank you for your writings.

John Rambo Thanks ! FYI the article has been updated, mostly at the end (final forecast) where I've skipped an important part.

In this series, I will walk you through a hands-on session to help you understand time series forecasting with panel data and stacked ensembles with R.

Cover photo by Mourizal Zativa on Unsplash Go to R-bloggers for R news and tutorials contributed by hundreds of R bloggers. Introduction This is the first of a series of 6 articles about time series forecasting with panel data and ensemble stacking w...

Le 16 juin 2026, Arthur Mensch, le patron emblématique de Mistral AI, a publié sur LinkedIn un message d’une rare solennité. Le discours officiel y célèbre, comme toujours, l’indépendance technologiqu

En janvier 2026, la directrice financière d'OpenAI a confirmé un chiffre que personne n'a relevé. Le triplement des revenus de l'entreprise — de 6,7 à 20 milliards de dollars — suit exactement le trip

En moins de trois mois, début 2026, Nvidia a injecté plus de 42 milliards de dollars dans l'écosystème IA. 30 milliards dans OpenAI. 10 milliards dans Anthropic. 2 milliards dans Nebius. Le reste disp

Un ingénieur. Soixante minutes. Un produit SaaS en production, utilisé par 450 marques.

Série "Couche 1 - Les Données"

Cover photo by Markus Spiske on Unsplash

Go to R-bloggers for R news and tutorials contributed by hundreds of R bloggers.

This is the sixth of a series of 6 articles about time series forecasting with panel data and ensemble stacking with R.

Through these articles I will be putting into practice what I have learned from the Business Science University training course 1 DS4B 203-R: High-Performance Time Series Forecasting", delivered by Matt Dancho. If you are looking to gain a high level of expertise in time series with R I strongly recommend this course.

The objective of this article is to learn how to build multi-level stacking ensembles with modeltime. In the figure below we start from the bottom by reminding us of each individual model or submodel performance from Part 4 (non-tuned models) and Part 5 (tuned models). Then we will define meta learners which learn from k-fold cross-validation predictions from all submodels. We can compare meta-learners' performance and select best meta-learners to be used for defining a weighted average ensemble to produce a final multi-level stacking model.

I assume you are already familiar with the following topics, packages and terms:

dplyr or tidyverse R packages

k-fold cross-validation

hyperparameter tuning from Part 4

average and weighted ensembles from Part 5

The following packages must be loaded:

# 01 FEATURE ENGINEERING

library(tidyverse) # loading dplyr, tibble, ggplot2, .. dependencies

library(timetk) # using timetk plotting, diagnostics and augment operations

library(tsibble) # for month to Date conversion

library(tsibbledata) # for aus_retail dataset

library(fastDummies) # for dummyfying categorical variables

library(skimr) # for quick statistics

# 02 FEATURE ENGINEERING WITH RECIPES

library(tidymodels) # with workflow dependency

# 03 MACHINE LEARNING

library(modeltime) # ML models specifications and engines

library(tictoc) # measure training elapsed time

# 04 HYPERPARAMETER TUNING

library(future)

library(doFuture)

library(plotly)

# 05 ENSEMBLES

library(modeltime.ensemble)

Leu us remind us of the performance of each individual model or submodel. We do not consider the ensemble models from Part 5.

# Load all calibration tables (tuned & non-tuned models)

> calibration_tbl <- read_rds("workflows_NonandTuned_artifacts_list.rds")

> calibration_tbl <- calibration_tbl$calibration

> calibration_tbl %>%

modeltime_accuracy() %>%

arrange(rmse)

# A tibble: 8 x 9

.model_id .model_desc .type mae mape mase smape rmse rsq

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 7 PROPHET W/ REGRESSORS Test 0.189 21.6 0.417 21.5 0.240 0.856

2 3 PROPHET W/ REGRESSORS - Tuned Test 0.189 21.6 0.418 21.5 0.241 0.857

3 4 PROPHET W/ XGBOOST ERRORS - Tuned Test 0.191 25.7 0.421 19.9 0.253 0.780

4 8 PROPHET W/ XGBOOST ERRORS Test 0.204 24.8 0.451 20.8 0.287 0.753

5 2 XGBOOST - Tuned Test 0.219 23.6 0.482 22.9 0.296 0.762

6 6 XGBOOST Test 0.216 25.0 0.476 22.4 0.299 0.747

7 1 RANGER - Tuned Test 0.231 26.1 0.509 24.6 0.303 0.766

8 5 RANGER Test 0.235 25.4 0.519 25.0 0.312 0.765

A stacking algorithm or meta-learner learns from predictions. The predictions come from k-fold cross-validations applied to each submodel. Once fed into the meta-learner tunable specification a hyperpameter tuning will be peformed for the meta-learner.

Remember, for non-sequential models you must perform a k-fold cross-validation and not a time series cross-validation. Let us get resampeld predictions with modeltime_fit_resamples(). Here, k=10 folds.

set.seed(123)

resamples_kfold <- training(splits) %>%

drop_na() %>%

vfold_cv(v = 10)

tic()

submodels_resamples_kfold_tbl <- calibration_tbl %>%

modeltime_fit_resamples(

resamples = resamples_kfold,

control = control_resamples(

verbose = TRUE,

allow_par = TRUE,

)

)

toc()

Parallel processing is set and toggled on by running the following commands:

# Parallel Processing ----

registerDoFuture()

n_cores <- parallel::detectCores()

plan(

strategy = cluster,

workers = parallel::makeCluster(n_cores)

)

In this article we will use 3 meta-learners: Random Forest, XGBoost, and SVM.

Create a stacking algorithm specification with ensemble_model_spec(). Within the meta-learner specification we must provide the tunable parameters, the number of folds, and the size of the grid. We will also set grid search control parameters by activating verbose and allowing parallel processing.

For all meta-learners specifications we will define a k=10 folds and a grid size of 20.

We perform tuning on 2 parameters: mtry and min_n.

We notice that the in-sample RMSE for the meta-learner is 0.125. Its performance on test data has RMSE = 0.230 and RSQ = 0.817.

tic()

set.seed(123)

ensemble_fit_ranger_kfold <- submodels_resamples_kfold_tbl %>%

ensemble_model_spec(

model_spec = rand_forest(

trees = tune(),

min_n = tune()

) %>%

set_engine("ranger"),

kfolds = 10,

grid = 20,

control = control_grid(verbose = TRUE,

allow_par = TRUE)

)

toc()

i Model Parameters:

# A tibble: 1 x 8

trees min_n .metric .estimator mean n std_err .config

<int> <int> <chr> <chr> <dbl> <int> <dbl> <chr>

1 1906 32 rmse standard 0.176 10 0.00225 Preprocessor1_Model02

i Prediction Error Comparison:

# A tibble: 9 x 3

.model_id rmse .model_desc

<chr> <dbl> <chr>

1 1 0.196 RANGER - Tuned

2 2 0.183 XGBOOST - Tuned

3 3 0.207 PROPHET W/ REGRESSORS - Tuned

4 4 0.179 PROPHET W/ XGBOOST ERRORS - Tuned

5 5 0.203 RANGER

6 6 0.203 XGBOOST

7 7 0.208 PROPHET W/ REGRESSORS

8 8 0.207 PROPHET W/ XGBOOST ERRORS

9 ensemble 0.125 ENSEMBLE (MODEL SPEC)

modeltime_table(

ensemble_fit_xgboost_kfold

) %>%

modeltime_accuracy(testing(splits))

# A tibble: 1 x 9

.model_id .model_desc .type mae mape mase smape rmse rsq

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1 ENSEMBLE (RANGER STACK): 8 MODELS Test 0.166 21.8 0.367 18.2 0.230 0.817

We perform tuning on 4 parameters: trees, tree_depth, learn_rate, loss_reduction.

We notice that the in-sample RMSE for the meta-learner is 0.0957. Its performance on test data RMSE = 0.251 and RSQ = 0.769.

tic()

set.seed(123)

ensemble_fit_xgboost_kfold <- submodels_resamples_kfold_tbl %>%

ensemble_model_spec(

model_spec = boost_tree(

trees = tune(),

tree_depth = tune(),

learn_rate = tune(),

loss_reduction = tune()

) %>%

set_engine("xgboost"),

kfolds = 10,

grid = 20,

control = control_grid(verbose = TRUE,

allow_par = TRUE)

)

toc()

# A tibble: 1 x 10

trees tree_depth learn_rate loss_reduction .metric .estimator mean n std_err .config

<int> <int> <dbl> <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

1 1717 8 0.0330 0.00876 rmse standard 0.180 10 0.00175 Preprocessor1_Model10

i Prediction Error Comparison:

# A tibble: 9 x 3

.model_id rmse .model_desc

<chr> <dbl> <chr>

1 1 0.196 RANGER - Tuned

2 2 0.183 XGBOOST - Tuned

3 3 0.207 PROPHET W/ REGRESSORS - Tuned

4 4 0.179 PROPHET W/ XGBOOST ERRORS - Tuned

5 5 0.203 RANGER

6 6 0.203 XGBOOST

7 7 0.208 PROPHET W/ REGRESSORS

8 8 0.207 PROPHET W/ XGBOOST ERRORS

9 ensemble 0.0957 ENSEMBLE (MODEL SPEC)

> modeltime_table(

ensemble_fit_xgboost_kfold

) %>%

modeltime_accuracy(testing(splits))

# A tibble: 1 x 9

.model_id .model_desc .type mae mape mase smape rmse rsq

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1 ENSEMBLE (XGBOOST STACK): 8 MODELS Test 0.182 23.9 0.401 19.7 0.251 0.769

We perform tuning on 3 parameters: cost, rbf_sigma, margin. Run ?svm_rbf for explanations.

We notice that the in-sample RMSE for the meta-learner is 0.172. Its performance on test data RMSE = 0.219 and RSQ = 0.823.

tic()

set.seed(123)

ensemble_fit_svm_kfold <- submodels_resamples_kfold_tbl %>%

ensemble_model_spec(

model_spec = svm_rbf(

mode = "regression",

cost = tune(),

rbf_sigma = tune(),

margin = tune()

) %>%

set_engine("kernlab"),

kfold = 10,

grid = 20,

control = control_grid(verbose = TRUE,

allow_par = TRUE)

)

toc()

# A tibble: 1 x 9

cost rbf_sigma margin .metric .estimator mean n std_err .config

<dbl> <dbl> <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

1 4.60 0.0110 0.0595 rmse standard 0.172 10 0.00222 Preprocessor1_Model07

i Prediction Error Comparison:

# A tibble: 9 x 3

.model_id rmse .model_desc

<chr> <dbl> <chr>

1 1 0.196 RANGER - Tuned

2 2 0.183 XGBOOST - Tuned

3 3 0.207 PROPHET W/ REGRESSORS - Tuned

4 4 0.179 PROPHET W/ XGBOOST ERRORS - Tuned

5 5 0.203 RANGER

6 6 0.203 XGBOOST

7 7 0.208 PROPHET W/ REGRESSORS

8 8 0.207 PROPHET W/ XGBOOST ERRORS

9 ensemble 0.172 ENSEMBLE (MODEL SPEC)

> modeltime_table(

ensemble_fit_svm_kfold

) %>%

modeltime_accuracy(testing(splits))

# A tibble: 1 x 9

.model_id .model_desc .type mae mape mase smape rmse rsq

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1 ENSEMBLE (KERNLAB STACK): 8 MODELS Test 0.160 21.8 0.352 18.0 0.219 0.823

The previous stacking approaches can be mutualized in a multi-level stack. We can combine meta-learners into a higher level of the stack which will be a normal (weighted) average ensemble as introduced in Part 5.

Below is a reminder of the previous stacking algorithms' performance:

modeltime_table(

ensemble_fit_ranger_kfold,

ensemble_fit_xgboost_kfold,

ensemble_fit_svm_kfold

) %>%

modeltime_accuracy(testing(splits)) %>%

arrange(rmse)

# A tibble: 3 x 9

.model_id .model_desc .type mae mape mase smape rmse rsq

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 3 ENSEMBLE (KERNLAB STACK): 8 MODELS Test 0.160 21.8 0.352 18.0 0.219 0.823

2 1 ENSEMBLE (RANGER STACK): 8 MODELS Test 0.166 21.8 0.367 18.2 0.230 0.817

3 2 ENSEMBLE (XGBOOST STACK): 8 MODELS Test 0.182 23.9 0.401 19.7 0.251 0.769

Let us now define a weighted average ensemble model from the stacking algorithms as we did in Part 5. We will apply the ranking technique to calculate the weights.

First we create the accuracy results table on which we apply the ranking technique for weigths calculation, then we create the weighted average ensemble model with ensemble_weighted() by applying the weights, and finally, we evaluate the model.

loadings_tbl <- modeltime_table(

ensemble_fit_ranger_kfold,

ensemble_fit_xgboost_kfold,

ensemble_fit_svm_kfold

) %>%

modeltime_calibrate(testing(splits)) %>%

modeltime_accuracy() %>%

mutate(rank = min_rank(-rmse)) %>%

select(.model_id, rank)

stacking_fit_wt <- modeltime_table(

ensemble_fit_ranger_kfold,

ensemble_fit_xgboost_kfold,

ensemble_fit_svm_kfold

) %>%

ensemble_weighted(loadings = loadings_tbl$rank)

> stacking_fit_wt %>%

modeltime_calibrate(testing(splits)) %>%

modeltime_accuracy() %>%

arrange(rmse)

# A tibble: 1 x 9

.model_id .model_desc .type mae mape mase smape rmse rsq

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1 ENSEMBLE (WEIGHTED): 3 MODELS Test 0.161 21.8 0.354 18.1 0.223 0.817

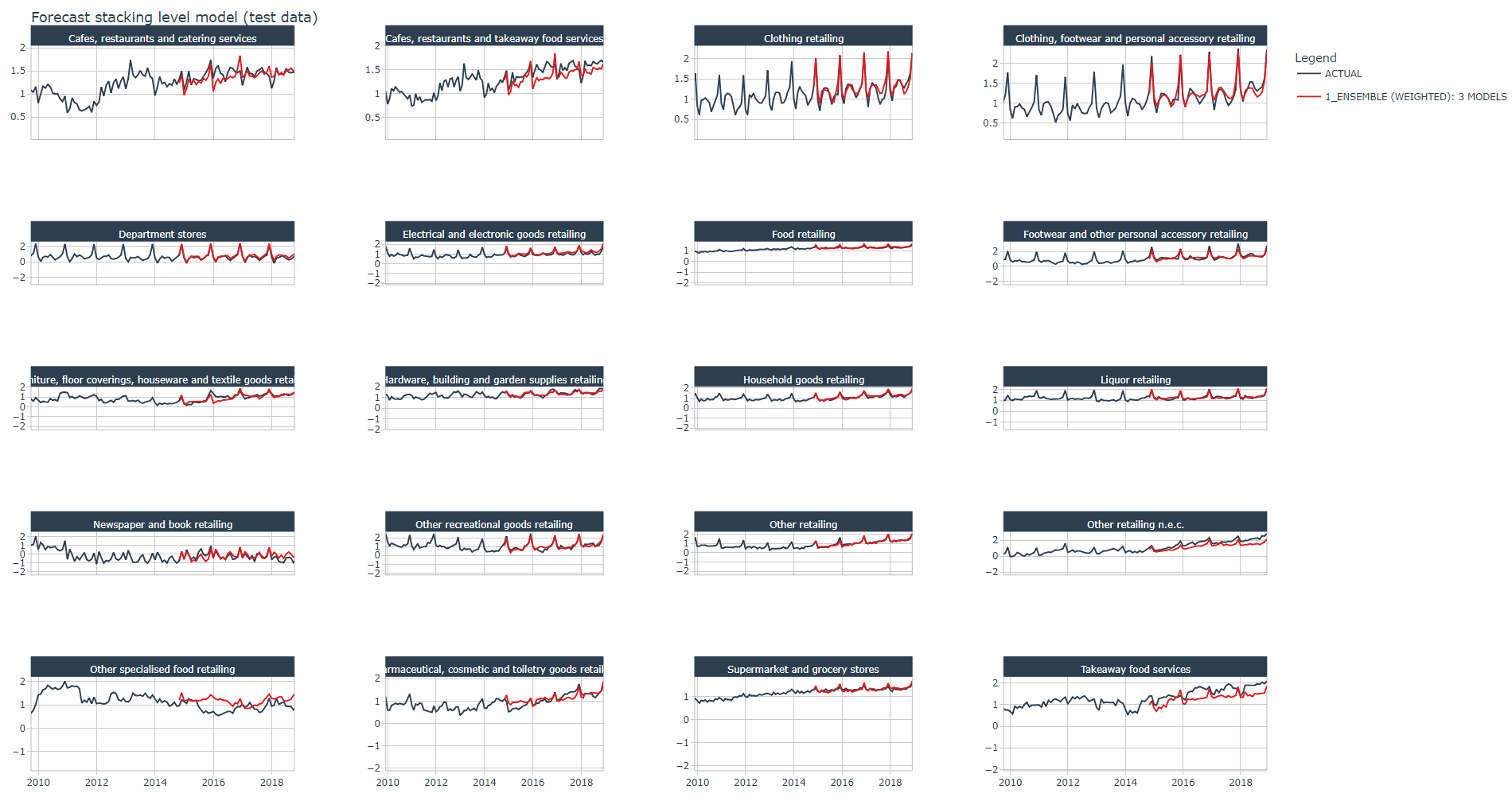

With RMSE = 0.223, the stacked ensemble algorithm outperformed all algorithms!

Below the stacked ensemble algorithm's forecast plot on the test dataset for all industries, it looks good ! except for one industry the model seems to follow pretty well the trend and spikes of the actual data.

calibration_stacking <- stacking_fit_wt %>%

modeltime_table() %>%

modeltime_calibrate(testing(splits))

calibration_stacking %>%

modeltime_forecast(

new_data = testing(splits),

actual_data = artifacts$data$data_prepared_tbl,

keep_data = TRUE

) %>%

group_by(Industry) %>%

plot_modeltime_forecast(

.facet_ncol = 4,

.conf_interval_show = FALSE,

.interactive = TRUE,

.title = "Forecast stacking level model (test data)"

)

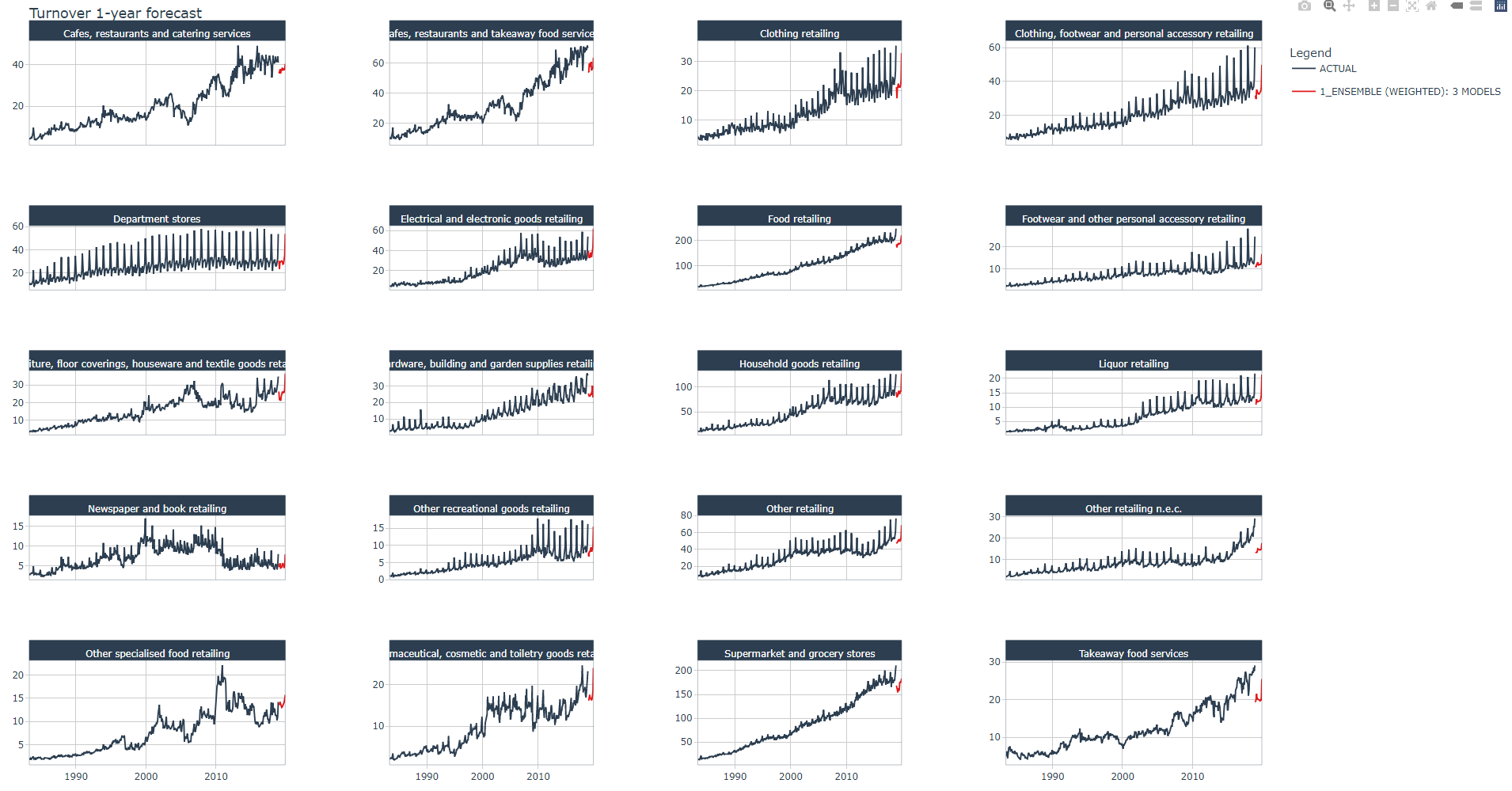

Let us now (finally!) perform the next 12 months Turnover forecast for all 20 industries as we promised in Part 1.

First, we must refit the stack-level weighted average model with the prepared dataset from Part 2. We do this with modeltime_refit().

Then we calculate the Turnover predictions over the next 12 months (values are still transformed). We do this with modeltime_forecast() and by setting new_data to the future dataset.

# Toggle ON parallel processing

plan(

strategy = cluster,

workers = parallel::makeCluster(n_cores)

)

# Refit the model on prepared dataset

tic()

set.seed(123)

refit_stacking_tbl <- calibration_stacking %>%

modeltime_refit(

data = artifacts$data$data_prepared_tbl,

resamples = artifacts$data$data_prepared_tbl %>%

drop_na() %>%

vfold_cv(v = 10)

)

toc()

# 12-month forecast calculations with future dataset

forecast_stacking_tbl <- refit_stacking_tbl %>%

modeltime_forecast(

new_data = artifacts$data$future_tbl,

actual_data = artifacts$data$data_prepared_tbl %>%

drop_na(),

keep_data = TRUE

)

# Toggle OFF parallel processing

plan(sequential)

We invert the Turnover values back to their original values with standardize_inv_vec() and expm1().

Finally, we plot the forecast for the next 12 months within the original scale of the Turnover measure.

lforecasts <- lapply(X = 1:length(Industries), FUN = function(x){

forecast_stacking_tbl %>%

filter(Industry == Industries[x]) %>%

#group_by(Industry) %>%

mutate(across(.value:.conf_hi,

.fns = ~standardize_inv_vec(x = .,

mean = artifacts$standardize$std_mean[x],

sd = artifacts$standardize$std_sd[x]))) %>%

mutate(across(.value:.conf_hi,

.fns = ~expm1(x = .)))

})

forecast_stacking_tbl <- bind_rows(lforecasts)

forecast_stacking_tbl %>%

group_by(Industry) %>%

plot_modeltime_forecast(.title = "Turnover 1-year forecast",

.facet_ncol = 4,

.conf_interval_show = FALSE,

.interactive = TRUE)

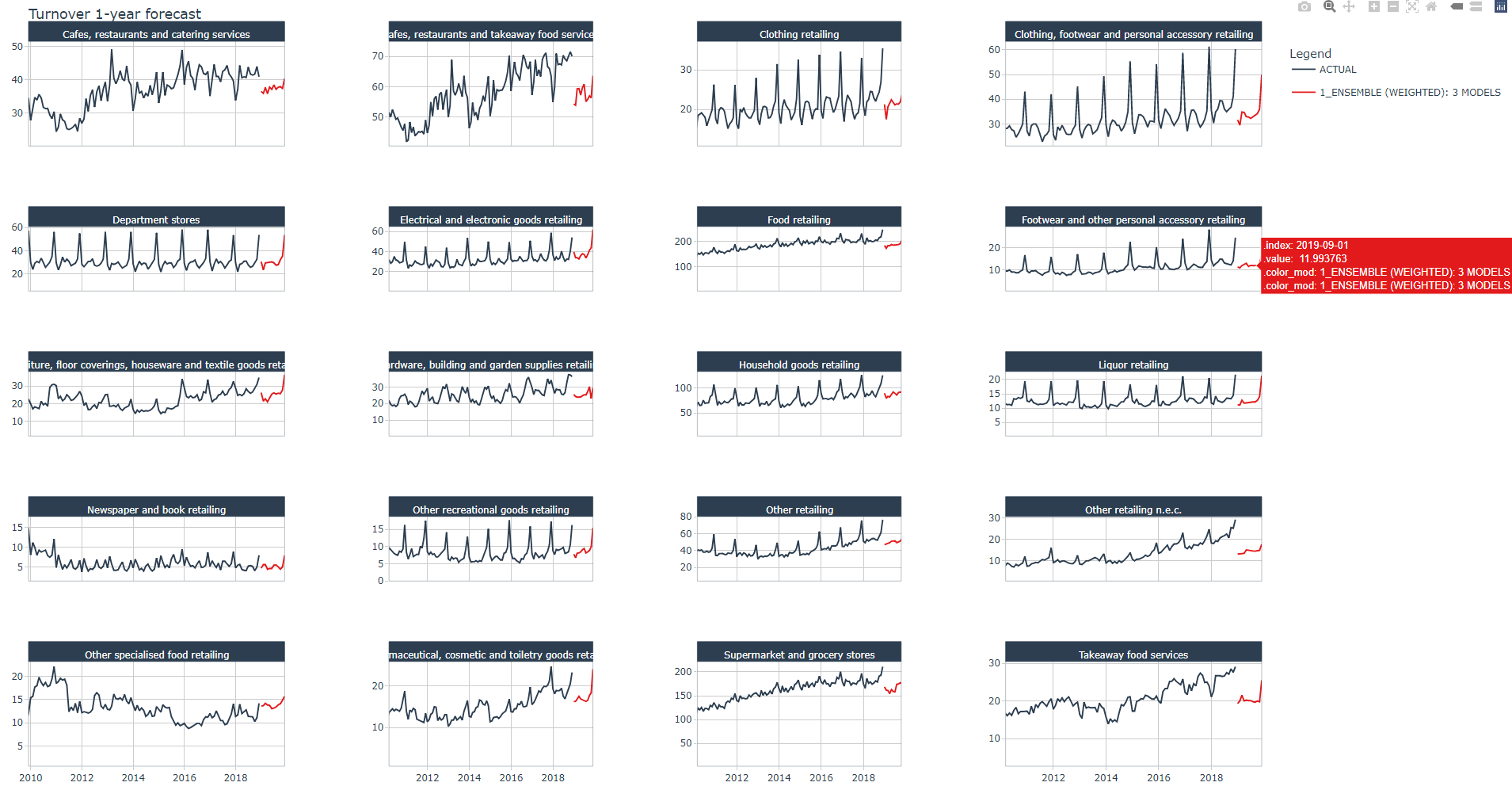

Below a zoomed view of the same plot

In this article you have learned how to implement stacked ensemble models. A stacking algorithm or meta-learner learns from predictions. The predictions come from k-fold cross-validations applied to each submodel. Once fed into the meta-learner tunable specification, a hyperpameter tuning will be peformed for the meta-learner.

We defined three meta-learners: SVM, Random Forest, and XGBoost from which we defined a weighted average ensemble model (stack-level) using the same method as explained Part 5.

The stacked ensemble algorithm outperformed all algorithms.

1 Dancho, Matt, "DS4B 203-R: High-Performance Time Series Forecasting", Business Science University