Cover photo by Mehdi Sepehri on Unsplash

Go to R-bloggers for R news and tutorials contributed by hundreds of R bloggers.

Introduction

This article is part of the series (Swarm) Portfolio Optimization. I assume you have read the Nonparametric VaR article or have solid notions about its calculation.

We will use the same 4-asset portfolio (MSFT, AAPL, GOOG, NFLX) as introduced in Nonparametric VaR.

We will

collect assets' prices, compute daily returns and clean data

format the daily returns tibble

compute weighted returns per asset

compute the mean of weighted returns per day

generate 1000 random 4-weight vectors or solutions or decision vectors

find the objective vectors corresponding to the non-nondominated solutions

visualize and distinguish the non-nondominated solutions from the dominated ones

As stated in the nonparametric VaR article, I like working with tibbles (and not time series R objects), that's why I use and recommend the tidyquant package.

Multi-objective optimization

Since the final goal of this series is the implementation of MOPSO, let us start with the mathematical concept behind multi-objective optimization as reminded in Mostaghim et al. paper [1]:

Our multi-objective problem

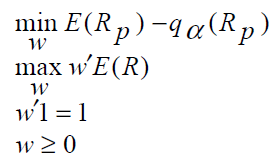

We want to use a multi-objective PSO approach to find VaR-efficient portfolios by solving the following optimization problem: [2]

where

Thus, we want to find a set of optimal solutions (weights w') to

minimize de Value-at-Risk (VaR), relative to the mean, of the portfolio

maximize the expected return of the portfolio

Our objective functions

We will define f1 as being the Value-at-Risk (VaR), relative to the mean, of the portfolio, and f2 as the expected return of the portfolio.

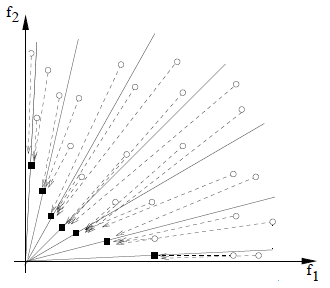

Finally, based on the mathematical explanation provided above we want to find the Pareto-optimal decision vectors (or weights) and their corresponding Pareto-optimal objective vector values (black squares in the figure below).

These Pareto-optimal decision vectors (or weights) are also called non-dominated solutions. In a MOPSO context they are also called archive-members.

Packages

Load the following packages:

library(PerformanceAnalytics)

library(quantmod)

library(tidyquant)

library(tidyverse)

library(timetk)

library(skimr)

library(plotly)

library(caret)

library(tictoc)

Collect prices, compute daily returns and clean data

This is the same code used in the Nonparametric VaR article.

# ASSETS

assets <- c("MSFT", "AAPL", "GOOG", "NFLX")

# TIME INTERVAL

end <- "2021-12-31" %>% ymd()

start <- end - years(5) + days(1)

# GET ASSETS' DAILY RETURNS

returns_daily_tbl <- assests %>%

tq_get(from = start, to = end) %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "daily") %>%

ungroup()

# PREPROCESSING - CLEAN

## Delete each asset first row (= 0)

rows_to_delete <- which(returns_daily_tbl$date == ymd("2017-01-03"))

returns_daily_tbl <- returns_daily_tbl[-rows_to_delete,]

Let us put the tibble in the right format by renaming the columns and converting the symbol column to factor, here below the corresponding custom function:

formatTibble <- function(tbl){

columnNames <- c("symbol", "date", "returns")

res <- tbl %>%

mutate(symbol = as.factor(symbol))

colnames(res) <- columnNames

return(res)

}

Get weighted returns

The next custom function getWeigthedReturns() multiplies a weight from the weight vector to its corresponding asset daily returns and outputs an updated tibble with new columns: weight and weighted.returns.

getWeigthedReturns <- function(tbl, vecA, vecW){

# Generate by-symbol tibble with weighted returns

# add by-symbol tibble to a list

lsymboltbl <- lapply(X = 1:length(vecA), function(x){

tbl %>%

filter(symbol == vecA[x]) %>%

mutate(weight = vecW[x]) %>%

mutate(weighted.returns = returns * weight)

})

# Bind symbol tibble by rows

res <- lsymboltbl %>%

bind_rows()

return(res)

}

Compute mean of weighted returns

Our goal here is to generate the same tibble (portfolio) from which we calculated the expected return and the "relative to the mean" VaR in the Nonparametric VaR article. Thus, we group by date and calculate the mean of daily returns of the 4 assets.

getMeanWeigthedReturns <- function(tbl){

res <- tbl %>%

group_by(date) %>%

summarise(mean.weighted.returns = mean(weighted.returns))

return(res)

}

Objective function f1: VaR

Although the custom function calculates both absolute and relative VaR, we consider only the "relative to the mean" VaR as the output of objective function f1.

objectiveFunction1 <- function(tbl, p = .99){

# Absolute VaR

absoluteVaR <- tbl %>%

tq_performance(Ra = mean.weighted.returns,

performance_fun = VaR,

p = p,

method = "historical")

# Relative VaR: E(Rp) - q(Rp)

relativeVaR <- mean(tbl\(mean.weighted.returns) - absoluteVaR\)VaR

return(list(VaR = list(abolute = absoluteVaR$VaR,

relative = relativeVaR)))

}

Objective function f2: Expected return

Since we apply a minimization for both objective functions, the objectiveFunction2() custom function outputs a negative value for the expected return.

objectiveFunction2 <- function(tbl){

# w'E(R)

res <- mean(tbl$mean.weighted.returns)

return(-res)

}

Other custom functions

We will generate 1000 random 4-weight solutions with the generateRandomWeightsVector() custom function. All four weights must sum to 1. I have also added a constraint to avoid generating 0-valued and 1-valued weights.

generateRandomWeightsVector <- function(n, min=.05, max=.75){

tmp <- runif(n = n, min = min, max = max)

nweights <- tmp/sum(tmp)

new_cols <- list()

for(x in 1:n) {

new_cols[[paste0("w_", x, sep="")]] = nweights[x]

}

res <- as_tibble(new_cols)

return(res)

}

We group the random solutions with their respective objective functions results in the same tibble with the following custom function:

getObjectiveFunctionsValues <- function(tbl, vecW){

new_cols <- list()

for(x in 1:length(vecW)) {

new_cols[[paste0("w_", x, sep="")]] = vecW[x]

}

res <- as_tibble(new_cols)

objf1val <- objectiveFunction1(tbl)

objf2val <- objectiveFunction2(tbl)

res <- res %>%

mutate(absVaR = objf1val\(VaR\)abolute) %>%

mutate(relVaR = objf1val\(VaR\)relative) %>%

mutate(expRet = objf2val) %>%

mutate(pAbsVaR = absVaR * 100) %>%

mutate(pRelVaR = relVaR * 100) %>%

mutate(pExpRet = expRet * 100)

return(res)

}

The tibble generated by the function above will be used to find the non-dominated solutions using the following custom function:

getNonDominated <- function(tbl) {

idxVar <- which(colnames(tbl) == "relVaR")

idxExpR <- which(colnames(tbl) == "expRet")

i <- order(tbl[, idxVar], tbl[, idxExpR], decreasing=FALSE)

frontier <- rep(0, length(i))

k <- 0;

y <- Inf

for (j in i) {

if (tbl[j, idxExpR] < y) {

frontier[k <- k+1] <- j

y <- tbl[j, idxExpR]

}

}

return(frontier[1:k])

}

Main R code

The code within the tictoc ran for 2 minutes, I have a Windows laptop, i5 CPU (8 vCores), 16GB RAM.

## 1. Create random particles tibble ----

NUMBER_OF_ASSETS = 4

NUMBER_PARTICLES = 1000

lrandomparticles <- lapply(X = 1:NUMBER_PARTICLES, function(x){

generateRandomWeightsVector(n = NUMBER_OF_ASSETS)

})

random_particles <- lrandomparticles %>%

bind_rows()

# 1000 random solutions

> random_particles

# A tibble: 1,000 x 4

w_1 w_2 w_3 w_4

<dbl> <dbl> <dbl> <dbl>

1 0.424 0.431 0.0569 0.0873

2 0.283 0.363 0.126 0.227

3 0.351 0.258 0.0496 0.341

4 0.266 0.218 0.431 0.0854

5 0.225 0.304 0.329 0.142

6 0.298 0.0952 0.409 0.198

7 0.190 0.197 0.424 0.189

8 0.335 0.310 0.264 0.0912

9 0.0437 0.430 0.274 0.252

10 0.0981 0.413 0.0400 0.449

# ... with 990 more rows

## 2. Generate particle & objective functions' results tibble ----

tic()

lparticlesObjFunResults <- lapply(1:NUMBER_PARTICLES, function(x){

weights <- as.numeric(random_particles[x,])

returns_daily_tbl %>%

formatTibble() %>%

getWeigthedReturns(vecA = assests, vecW = weights) %>%

getMeanWeigthedReturns() %>%

getObjectiveFunctionsValues(vecW = weights) %>%

mutate(sharpe = expRet/relVaR)

})

toc()

particlesObjFunResults <- lparticlesObjFunResults %>%

bind_rows()

> particlesObjFunResults

# A tibble: 1,000 x 11

w_1 w_2 w_3 w_4 absVaR relVaR expRet pAbsVaR pRelVaR pExpRet sharpe

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 0.424 0.431 0.0569 0.0873 -0.0109 0.0113 -0.000396 -1.09 1.13 -0.0396 0.0352

2 0.283 0.363 0.126 0.227 -0.0106 0.0110 -0.000387 -1.06 1.10 -0.0387 0.0352

3 0.351 0.258 0.0496 0.341 -0.0107 0.0111 -0.000390 -1.07 1.11 -0.0390 0.0353

4 0.266 0.218 0.431 0.0854 -0.0110 0.0113 -0.000355 -1.10 1.13 -0.0355 0.0314

5 0.225 0.304 0.329 0.142 -0.0108 0.0112 -0.000367 -1.08 1.12 -0.0367 0.0329

6 0.298 0.0952 0.409 0.198 -0.0106 0.0109 -0.000353 -1.06 1.09 -0.0353 0.0324

7 0.190 0.197 0.424 0.189 -0.0108 0.0111 -0.000355 -1.08 1.11 -0.0355 0.0319

8 0.335 0.310 0.264 0.0912 -0.0108 0.0111 -0.000373 -1.08 1.11 -0.0373 0.0336

9 0.0437 0.430 0.274 0.252 -0.0107 0.0110 -0.000376 -1.07 1.10 -0.0376 0.0340

10 0.0981 0.413 0.0400 0.449 -0.0112 0.0116 -0.000396 -1.12 1.16 -0.0396 0.0340

# ... with 990 more rows

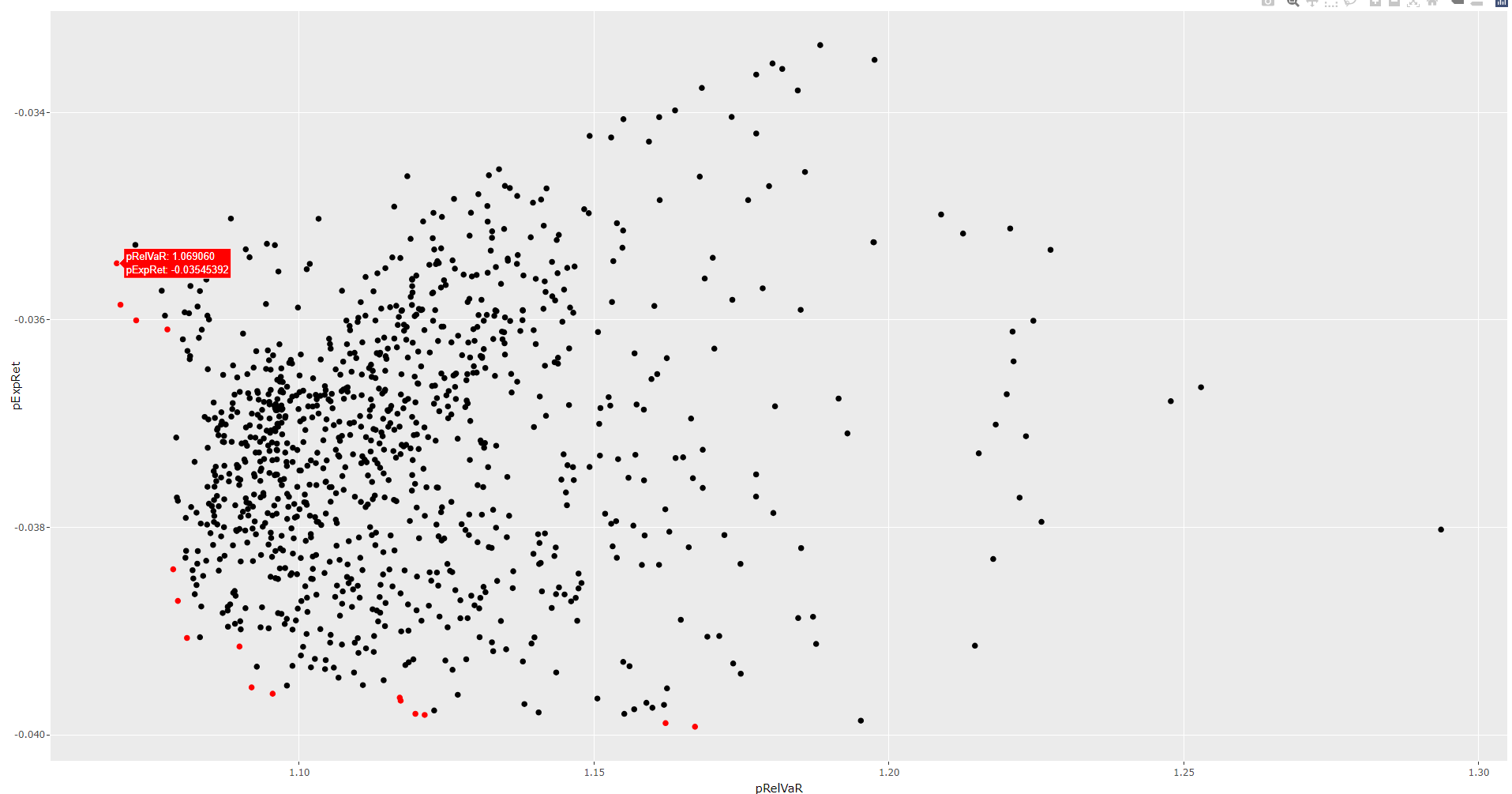

ndidx <- getNonDominated(tbl = particlesObjFunResults)

gp <- ggplot() +

geom_point(particlesObjFunResults[ndidx,], mapping = aes(x = pRelVaR, y = pExpRet), color = "red") +

geom_point(particlesObjFunResults[-ndidx,], mapping = aes(x = pRelVaR, y = pExpRet), color = "black")

ggplotly(gp)

Be reminded that the objective function f2 outputs negative values for the portfolio expected returns (because we consider a minimization problem, see the figure of Pareto-optimal objective vector at the beginning of the article). Thus, we are actually displaying the frontier upsides down.

Below you will find the 16 non-dominated solutions (red points) along with their corresponding VaR (%) and expected return (%) results (expressed in percentage), keeping the negative sign of the expected return (%).

In the Nonparametric VaR article we considered an equally distributed weight set (25% weight for each asset) and obtained an expected return of 0.032% and a relative VaR of 1.08%. We see that the first 3 non-dominated solutions below provide a higher expected return (ignore the negative sign) with less risk.

> particlesObjFunResults[ndidx,] %>%

select(w_1, w_2, w_3, w_4, pRelVaR, pExpRet) %>%

arrange(pRelVaR)

# A tibble: 16 x 6

w_1 w_2 w_3 w_4 pRelVaR pExpRet

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 0.313 0.0748 0.386 0.226 1.07 -0.0355

2 0.310 0.110 0.354 0.225 1.07 -0.0359

3 0.283 0.138 0.347 0.232 1.07 -0.0360

4 0.345 0.0844 0.318 0.252 1.08 -0.0361

5 0.447 0.193 0.101 0.259 1.08 -0.0384

6 0.359 0.256 0.0869 0.298 1.08 -0.0387

7 0.420 0.338 0.0818 0.161 1.08 -0.0391

8 0.458 0.310 0.0629 0.169 1.09 -0.0391

9 0.378 0.394 0.0476 0.181 1.09 -0.0395

10 0.302 0.419 0.0466 0.233 1.10 -0.0396

11 0.244 0.481 0.0645 0.211 1.12 -0.0396

12 0.168 0.527 0.0759 0.230 1.12 -0.0397

13 0.217 0.446 0.0313 0.305 1.12 -0.0398

14 0.378 0.453 0.0408 0.128 1.12 -0.0398

15 0.175 0.600 0.0810 0.144 1.16 -0.0399

16 0.105 0.604 0.0752 0.216 1.17 -0.0399

Conclusion

In this article I wanted to illustrate the notion of non-dominated solutions applied to a portofolio optimization use case. Here we started by generating a random set of 1000 weight vectors in order to find the non-dominated solutions among this set of 1000 weight vectors. Our utimate goal will be to generate these weight vectors and non-dominated solutions with the MOPSO algorithm, but first we will explain other notions such as finding good local guides with the Sigma method [1].

References

[1] Mostaghim S., Teich J., « Strategies for Finding Local Guides in Multi-objective Particle Swarm Optimization (MOPSO) »

[2] Alfaro Cid E. et al., « Minimizing value-at-risk in a portfolio optimization problem using a multiobjective genetic algorithm », International Journal of Risk Assessment and Management, 2011